The United States won’t have a digital dollar - not now, not under this administration, and maybe not for a long time. In early 2025, President Donald Trump signed Executive Order 14178, shutting down every federal effort to build a central bank digital currency (CBDC). The so-called "digital dollar," sometimes called FedCoin, is officially off the table. This wasn’t a delay. It wasn’t a pause. It was a full stop.

Just two years earlier, the Biden administration had made CBDC research a top priority. Executive Order 14067 in 2022 told the Federal Reserve and Treasury Department to move fast - explore designs, test systems, consult experts, and prepare for possible rollout. The U.S. had already formed a high-level task force with the White House, Treasury, National Security Council, and Federal Reserve all working together. Nellie Liang, then a top Treasury official, called it a "coordinated, whole-of-government effort" to shape the future of money.

Then came the reversal. In one executive order, every working group was dissolved. All funding for CBDC pilots was cut. Federal Reserve Chair Jerome Powell publicly confirmed he would never issue a CBDC while he’s in office. The message was clear: the U.S. government is walking away from digital currency.

Why the U.S. Is the Only Major Economy Doing This

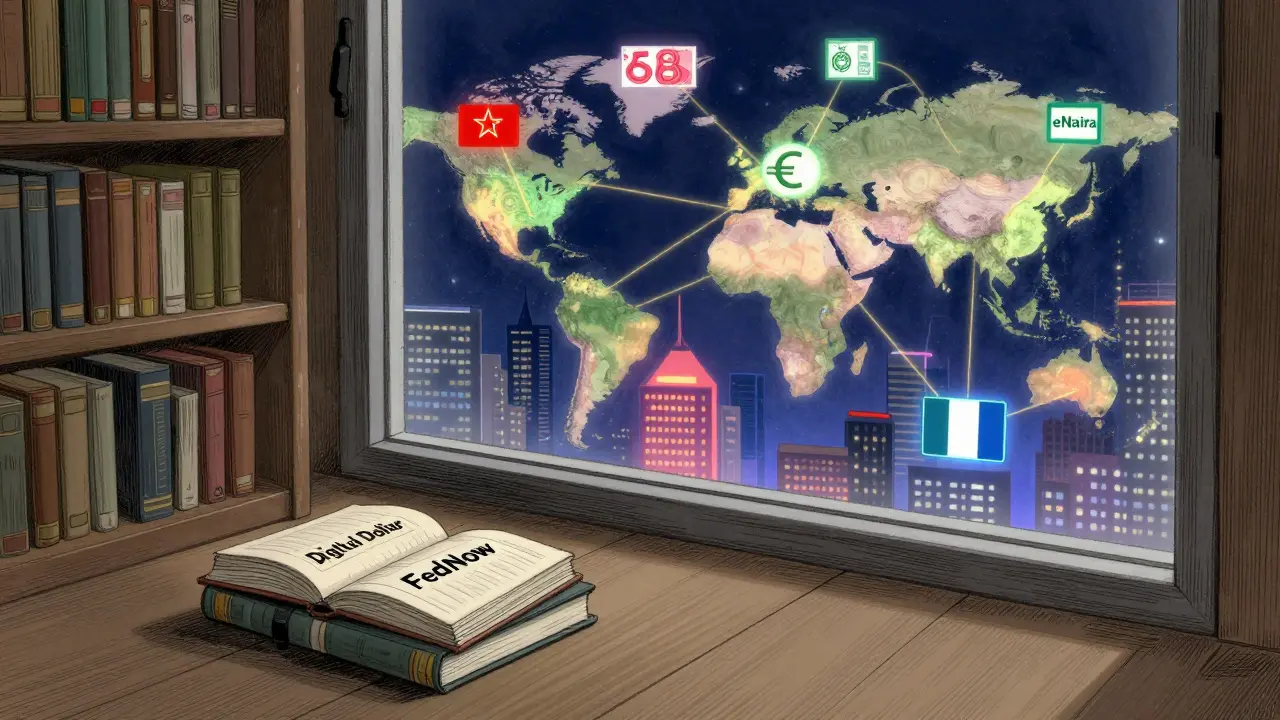

While the U.S. pulled the plug, the rest of the world kept going. As of early 2025, 134 countries and currency unions are actively working on CBDCs. That’s up from 114 just two years ago. Of those, 72 are in advanced stages - building, testing, or launching. Fifty-three countries are running live pilots. Eleven have already rolled out full CBDCs, including Nigeria, Jamaica, the Bahamas, and Zimbabwe.

Even within the G-20 - the world’s most powerful economies - only the U.S. has completely halted progress. Every other member, from Germany and Japan to Brazil and India, is moving forward. The European Central Bank is deep into its digital euro pilot, aiming for a possible launch by 2026. China’s digital yuan has been in use for years, processing billions in transactions annually. Australia, Turkey, and South Korea are all testing their own versions.

The U.S. isn’t just behind - it’s alone. And that matters. Money doesn’t just move within borders anymore. Cross-border payments, trade settlements, and financial diplomacy are shifting to digital rails. By refusing to build its own, the U.S. is letting others write the rules.

What Was Lost: Infrastructure, Innovation, and Influence

The U.S. didn’t start from scratch. By 2024, it had spent over $120 million on CBDC research. The Fed had tested multiple technical architectures. Treasury had drafted legal frameworks. The interagency team had mapped out how a digital dollar could integrate with existing payment systems like FedNow. They even explored how programmability - the ability to set rules on how money is spent - could help deliver stimulus checks automatically or restrict spending to specific goods.

But none of that matters now. The code was never written. The pilots were never scaled. The legal guardrails were never finalized. All that work vanished overnight. And with it went the chance for the U.S. to shape global standards.

Other countries are building CBDCs to reduce reliance on the U.S. dollar. China, Russia, and India are creating alternatives to SWIFT. The EU wants more control over its financial system. The U.S. had the chance to lead this transition - to set security standards, privacy norms, and interoperability rules. Instead, it stepped aside.

Private Money Is Filling the Void - But It’s Not the Same

Without a government-backed digital dollar, private companies are rushing in. Fnality International, a consortium backed by State Street and other big banks, is developing a private digital USD token. It’s not a CBDC. It’s not issued by the Fed. It’s not legal tender. But it’s designed to settle large transactions between institutions using blockchain technology.

State Street has said that having a "high-credit, quality digital cash asset" is critical for institutional investors to enter the digital asset space. But here’s the catch: private tokens aren’t backed by the full faith and credit of the U.S. government. They’re backed by a group of banks. That’s a different kind of trust.

And while private stablecoins like USDC and USDT dominate retail crypto markets, they’re still vulnerable to regulatory crackdowns, corporate failure, or loss of reserve backing. A CBDC would have been immune to that. It would have been digital cash - just like a $20 bill, but in app form.

Why Did This Happen? Surveillance, Politics, and Fear

There’s no official reason given for the halt. But clues are everywhere.

For years, critics warned that a U.S. CBDC could become a tool for mass financial surveillance. Banks already file over 26 million suspicious activity reports every year. The government already tracks spending through tax forms, bank reporting, and credit card data. A digital dollar would have made that tracking easier, faster, and more complete.

That’s a scary thought for many Americans. In a country where civil liberties are already under pressure - with asset forfeiture laws allowing police to seize cash without charges - the idea of a government-controlled digital wallet triggered deep distrust.

Political ideology played a role too. The current administration sees private crypto and stablecoins as the answer to financial innovation, not government-run systems. They argue that regulation, not issuance, is the path forward. They want clarity on stablecoins, not a new form of money.

But that’s a gamble. Private money doesn’t solve the same problems as a CBDC. It doesn’t guarantee universal access. It doesn’t ensure payment efficiency for the unbanked. It doesn’t give the government tools to respond quickly to economic crises.

The Global Impact: Who Wins When the U.S. Walks Away?

By 2025, the global value of CBDC transactions is projected to hit $213 billion - more than double what it was in 2023. Countries using CBDCs are seeing faster settlements, lower costs, and better control over monetary policy. Central banks in emerging markets are using CBDCs to fight inflation and reduce dependency on the U.S. dollar.

Meanwhile, the U.S. is stuck. Its financial system still relies on legacy infrastructure. Cross-border payments take days. Small businesses pay high fees. People without bank accounts can’t access digital payments easily. And now, the U.S. has chosen not to fix it.

Other nations are already planning CBDC interoperability - systems where digital euros, digital yuan, and digital yen can trade directly with each other. The U.S. dollar will still be the world’s reserve currency. But its dominance won’t last forever. And if the U.S. doesn’t have a digital version of its own currency, it won’t be able to compete in the next phase of global finance.

What Comes Next?

The digital dollar is dead. But the conversation isn’t over.

Private stablecoins will keep growing. Big banks will keep pushing for regulatory clarity. Congress may pass laws to govern crypto assets - but they won’t create a digital dollar. The Federal Reserve has said it won’t pursue one. The Treasury has no plans to revive the task force.

For now, the U.S. is betting that private innovation will fill the gap. But history shows that when it comes to money, trust matters more than speed. And trust in private companies is not the same as trust in the government - especially when that government is the issuer of the world’s most important currency.

The U.S. has chosen a different path. Whether it’s the right one won’t be clear for years. But one thing is certain: the world is moving forward. And the U.S. is standing still.

Akhil Mathew

January 28, 2026 AT 12:09The U.S. just handed China and the EU the keys to the next financial system and we're acting like it's no big deal. We spent a decade building the dollar's global dominance, now we're throwing it away because someone got scared of surveillance? We're not just falling behind-we're voluntarily stepping off the train.

Ramona Langthaler

January 29, 2026 AT 12:35good riddance to fedcoin lol the gov just wants to track every coffee you buy and freeze your account if you say the wrong thing on twitter. free money dont need a government app to work

Rico Romano

January 29, 2026 AT 17:45It's not that we're behind-it's that we're smarter. The U.S. has the most resilient financial infrastructure in history. Why replace a system that works with a brittle, hackable, centrally controlled digital token? The rest of the world is rushing into a trap. We're the only ones with the discipline to pause and ask: is this really necessary?

Joshua Clark

January 30, 2026 AT 09:13Look, I get the surveillance fears, but let’s be real-our financial system is already under constant surveillance. Credit card companies, banks, tax agencies, even your smart fridge probably knows what you bought last Tuesday. A CBDC wouldn’t make it worse-it would make it transparent, accountable, and secure. Right now, private stablecoins are the Wild West. No FDIC insurance. No legal tender status. No consumer protections. We’re trading a regulated public option for a corporate gamble. And for what? A political slogan?

The Fed had a solid framework. They were testing interoperability with FedNow. They were exploring programmable payments for disaster relief. We could’ve had digital SNAP benefits that couldn’t be spent on alcohol or cigarettes. We could’ve cut cross-border settlement times from days to seconds. Instead, we just… stopped. And now we’re letting private banks dictate the future of money. That’s not freedom. That’s surrender.

Brandon Vaidyanathan

January 30, 2026 AT 22:20OMG this is the most terrifying thing that’s ever happened in finance 😭 The U.S. is literally handing over global monetary power to China and Russia. Imagine a world where your paycheck is paid in digital yuan because the U.S. dollar is stuck in 1998. We’re not just losing tech-we’re losing sovereignty. And for what? So some guy on Reddit can say "they’re tracking me"? 🤦♂️

Gareth Fitzjohn

February 1, 2026 AT 01:25Interesting development. The U.S. has always been cautious with financial innovation. That’s not necessarily a bad thing. But the speed at which other nations are moving does raise questions about long-term competitiveness. The question isn’t whether a CBDC is good or bad-it’s whether the U.S. can afford to not have one.

Katie Teresi

February 1, 2026 AT 20:10They're coming for your cash and you're celebrating? You think private stablecoins are safer? USDC froze accounts during the bank run. You think a bank consortium is less creepy than the Fed? Wake up. This isn't freedom. It's corporate feudalism.

Moray Wallace

February 2, 2026 AT 00:53I appreciate the concerns about surveillance, but I wonder if the real issue is the lack of public dialogue. We never really had a national conversation about what a digital dollar would mean. Was it ever truly a democratic decision, or just a bureaucratic project that got shut down by political whim?

Dahlia Nurcahya

February 3, 2026 AT 11:05Hey, I get the fear-but let’s not throw the baby out with the bathwater. A CBDC doesn’t have to mean surveillance. It could mean instant disaster relief, lower fees for small businesses, and financial access for the 5% of Americans still unbanked. We can build privacy into it. We can make it opt-in. We can limit data collection. But we won’t if we just say no. The U.S. can lead on this-let’s not be the country that chose fear over innovation.

William Hanson

February 5, 2026 AT 03:20Wow. So we spent 120 million dollars and then just deleted everything? That’s not policy. That’s a temper tantrum. The Fed had the tech. The Treasury had the legal framework. The White House had the task force. And then some guy in a suit said "nah" and hit delete. This isn’t leadership. This is laziness with a flag.

Lori Quarles

February 6, 2026 AT 09:21China’s digital yuan is already being used in Africa and Latin America. They’re offering it as an alternative to the dollar. We’re sitting here like we’re protecting liberty while they’re building the future. If you think the U.S. dollar will always rule, you’re not paying attention. This isn’t about tech-it’s about power. And we’re giving it away.

Jeremy Dayde

February 6, 2026 AT 13:12It’s funny how people act like CBDCs are some kind of dystopian nightmare when the reality is most of us already live in a world where every transaction is tracked. Your Amazon purchases. Your Netflix habits. Your credit card data. Your phone location. The government already has way more info than a digital dollar would ever give them. The real question is why we’re okay with private corporations having all this data but freak out when the Fed might have it. Who do you trust more-JPMorgan or the Federal Reserve? I mean really. Think about it.

Steven Dilla

February 8, 2026 AT 06:23Bro the Fed could’ve made a CBDC with zero surveillance features 🤯 Like literally turn off tracking. Just make it digital cash. But nooo we had to turn it into a political football. Now private banks are gonna make their own version and charge us 5% to send money to Mexico. 💸😭

josh gander

February 9, 2026 AT 15:31Let’s not forget the real win here: we avoided turning money into a loyalty program. Imagine getting a "stimulus coupon" that only works at Walmart. Or your child’s allowance gets blocked if they try to buy a video game. A CBDC could’ve been a nightmare of micro-control disguised as efficiency. I’d rather have a messy, slow, private crypto ecosystem than a government-run financial puppet show. We didn’t lose-we dodged a bullet.

christal Rodriguez

February 9, 2026 AT 23:19Actually, the dollar will remain dominant because it's backed by oil, not code. CBDCs are a distraction. The real threat is inflation. Not digital cash.

Calvin Tucker

February 11, 2026 AT 21:52The premise of this article is flawed. A CBDC is not a necessary component of monetary sovereignty. The U.S. dollar’s status is rooted in legal enforceability, market depth, and institutional credibility-not technological infrastructure. The rest of the world is chasing novelty. The U.S. is maintaining stability. There is no moral or economic imperative to digitize currency.

Gustavo Gonzalez

February 13, 2026 AT 04:44So you’re saying we’re behind because we didn’t build a government app to track your grocery spending? What’s next? Mandatory CBDC-linked social credit scores? You know what’s more dangerous than a digital dollar? People who think the government should control money. Wake up. This isn’t innovation. It’s control.

Gavin Francis

February 14, 2026 AT 21:02Man I just want to send money to my cousin in Nigeria without paying $40 in fees and waiting 3 days. If a digital dollar could fix that, I don’t care if the Fed knows I bought tacos on Tuesday. 😅 Let’s just make it work!

Gary Gately

February 16, 2026 AT 14:37cbdc bad gov tracking bad but also why is everyone using usdc when its backed by blackrock? like… the gov is the bad guy but private banks are fine? idk man

Tom Sheppard

February 17, 2026 AT 21:43As a Canadian, I’m watching this with awe. We’re building our own digital loonie, and honestly? It’s not about control-it’s about efficiency. Our seniors need better access. Small businesses need faster payouts. We’re not trying to spy on anyone-we’re trying to fix a broken system. The U.S. has the resources to lead. Why are you choosing to sit this one out?

Aaron Poole

February 18, 2026 AT 01:57Let’s be honest-the real issue isn’t surveillance. It’s trust. People don’t trust the Fed anymore. They don’t trust Congress. They don’t trust banks. And honestly? Neither do I. But instead of building a CBDC that fixes that-like transparent audits, user-controlled privacy, and real consumer rights-we just gave up. The solution isn’t to abandon innovation. It’s to demand better. A digital dollar could’ve been a tool for accountability, not control. We had the chance to fix the system. We chose to walk away.

Andrea Demontis

February 18, 2026 AT 04:59Money has always been a social contract. It’s not about the technology-it’s about who we agree to trust. For centuries, we trusted gold. Then we trusted paper backed by a king. Then we trusted a central bank backed by the full faith of a nation. Now we’re being asked to trust code, algorithms, and private corporations. The U.S. didn’t reject a digital dollar. It rejected the idea that money should be a public good. That’s a philosophical shift. And it’s bigger than any executive order.

Joseph Pietrasik

February 19, 2026 AT 15:22you think the fed wouldnt use cbdc to tax you on savings? lol no thanks

Raju Bhagat

February 21, 2026 AT 09:42Bro the whole world is moving to digital money and we’re still arguing about whether the government will spy on us? I mean… we already live in a surveillance state. At least a CBDC would let me send money to my family in India without paying 10% in fees. This isn’t freedom. This is just being lazy. 🤷♂️